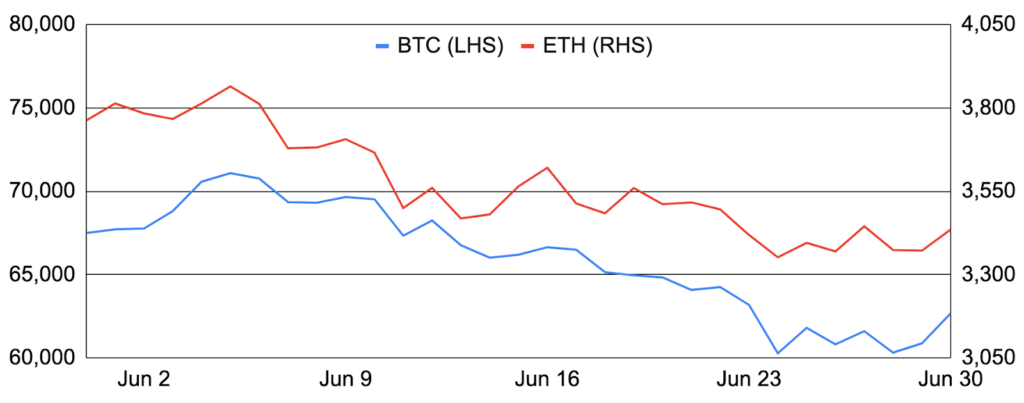

Bitcoin and Ethereum

Bitcoin entered June around $67,500 and fell 7% during the month to finish at ~$62,700. Bitcoin moved higher to start the month on $1.8b of inflows into the US spot Bitcoin ETFs, but soon gave way to worsening ETF flows, a mid-month hawkish Fed meeting, German government selling, and most notably, the Mt Gox trustee announcing that creditors will start to receive repayments beginning in July. The falling price caused the Fear & Greed Index to slip into Fear territory, network hashrate to fall by 6% during the month, and for active addresses to hit a five year low. Nevertheless, there were still notable/positive items during the month, including: Strike launched operations in the UK, Deutsche Telekom announced intentions to mine Bitcoin, total Bitcoin L2 TVL breached $2b, DeFi Technologies revealed plans to stake $100m BTC on Core Chain, BVM launched a ZK rollup service, StarkWare announced intentions to scale Bitcoin with ZK proofs, Ark formed a new company for Bitcoin payments, and Donald Trump negotiated with organizers to potentially attend the Bitcoin 2024 convention in July.

Ethereum largely mirrored Bitcoin, falling 9% during the month after entering June around $3,750 and finishing at ~$3,450. ETH’s underperformance occurred despite anticipation for its coming US spot Ethereum ETFs, which continue to progress and will likely launch in the back half of July, as well as the SEC’s closing of its investigation into Ethereum 2.0. During the month, ETH’s supply grew by ~50,000 ETH, or 0.5% annualized, as staking rewards outpaced ETH burned. Notably, ETH has been inflationary since April, as activity continues to shift to L2s and with Dencun enabling L2 data to be posted back to Ethereum via blobs. In addition, Ethereum devs confirmed the inclusion of several EIPs in its next major upgrade, dubbed Pectra and expected in 1Q25, including EIP-7251 (known as max effective balance, allowing validators to carry a balance of up to 2,048 ETH to consolidate validators and cut down on messaging requirements), EIP-7594 (adds PeerDAS, a first step in data availability sampling to further improve data availability throughput), and EIP-7702 (designed to streamline the integration of account abstraction). Additionally, the combined TPS for Ethereum and its L2s hit a new all-time high, EigenLayer’s TVL surpassed $20b for the first time, and Paradigm released the Ethereum execution client Reth 1.0. Finally, there were several notable L2 developments including: Arbitrum greenlit its BOLD challenge resolution protocol positioning it for stage 2 decentralization; Optimism released fault proofs on OP Mainnet to reach stage 1 decentralization; Taiko enabled permissionless sequencing and proving; Celestia launched Blobsteam on Ethereum mainnet to enable Ethereum L2s to permissionlessly use Celestia data availability; ZKsync announced a new Elastic Chain interoperability solution; and, Polygon created a new 1b POL grants program.

BTC and ETH

Source: Santiment, GSR.

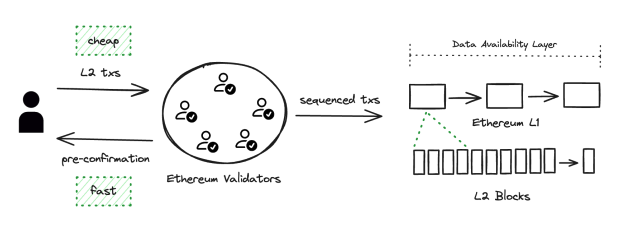

Based Rollups for a Unified Layer 2

Conceived in 2013 by Vitalik Buterin and launched in mid-2015, Ethereum revolutionized blockchain technology and cryptocurrencies forever by enabling nodes to process general purpose code, known as smart contracts, to add programmability and arbitrary computation to the blockchain. While incredibly novel, Ethereum optimized for decentralization and security that when combined with early design decisions and a philosophical preference for low hardware requirements, has led to comparatively low throughput and periodic congestion/fee spikes during times of significant activity. To remedy, Vitalik Buterin proposed his beautiful rollup-centric roadmap that pushes compute off Ethereum mainnet to execute transactions off-chain (ie. on rollups) before proving to Ethereum that the transactions (state transitions) were processed validly. Such a setup significantly increases throughput as transaction validation is more efficient than running the transactions themselves, and enables rollups to inherit many of the security properties of Ethereum mainnet itself (in addition to transforming Ethereum from the world computer to the world settlement layer). However, such a setup also fragmented rollup state and liquidity.

First proposed by Justin Drake in early 2023, one solution that is gaining considerable momentum is based rollups and preconfirmations. Unlike typical rollups that rely on a single, centralized sequencer to choose which transactions are included in a block and in what order, based rollups use Ethereum mainnet validators to select and order transactions, essentially making Ethereum mainnet the shared sequencer for all based rollups and enabling atomic interoperability not only between the based rollup and mainnet, but also between the based rollups themselves. This, however, only solves part of the problem, as Ethereum’s 12 second block time is incongruent with the shorter block times of rollups. This is where preconfirmations come in, which allow an Ethereum validator to pledge ETH as a bond and promise to include an L2’s transaction in the next Ethereum block, adding economic security behind based rollup transaction inclusion and creating a notion of finality that can be extremely fast, such as 100-200 milliseconds. And while based rollups do not order their own transactions and therefore lose the ability to extract MEV, there are reasons to believe their MEV opportunity will fall regardless over time. More importantly, based rollups inherit the liveness, censorship resistance, credible neutrality, and real-time settlement guarantees of Ethereum itself, and atomic composability should enable based rollups to garner more execution than would otherwise be the case. While based rollups and preconfirmations are technically complex and the debate continues, projects continue to build with a based rollup world in mind, as evidenced by Taiko launching on Ethereum mainnet as the first based (contestable) rollup, Espresso building based rollup solutions like MEV redistribution and enhanced preconfirmations, and Puffer Finance leveraging its Puffer validator set to create a based app-chain ecosystem.

Based Sequencing

Source: Puffer Finance, GSR.

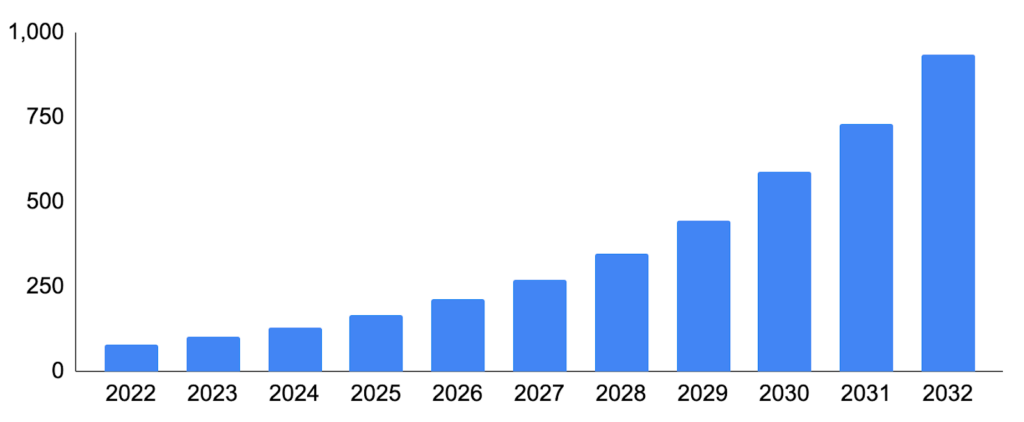

Bitcoin’s Pivoting Miners

The economics of Bitcoin mining have been challenged since the recent Bitcoin halving, which saw block rewards move from 6.25 to 3.125 BTC per block in April. Indeed, due to a combination of the lowered block reward, rising network difficulty, and the recent decline in Bitcoin’s price, the Hashprice Index, which quantifies the revenue potential of a unit of Bitcoin mining hashrate, is sitting at an all-time low. And though public miners , who possess a lower all-in cost per coin than the network as a whole, moved towards more efficient rigs and shored up their balance sheets prior to the halving, many continued to look for ways to diversify revenue sources amidst the current financial backdrop.

Enter High Performance Computing (HPC) and more specifically AI, with its skyrocketing demand for data centers that can meet its immense and growing computational needs. And with Bitcoin miners’ access to power, data center infrastructure, and hosting expertise, it’s no wonder that a number of miners are offering HPC and AI hosting services. To be sure, the pivot to HPC/AI services isn’t simple, as not all data centers can be modified for AI-related use cases, and there are significant time and capital investment required for the ones that can, with AI data centers having more expensive build costs, higher power density requirements, greater bandwidth needs, and more specialized hardware relative to Bitcoin mining. Despite this, the benefits for both parties are large, with AI companies able to access computing services faster than they may otherwise have been able to amidst the constrained supply of available high-power sites, and miners able to add a growing, low volatility, and high margin revenue source to complement their existing mining businesses. Already, there have been notable HPC initiatives such as from Iris Energy and Bit Digital, and June saw a continuation of this trend. Core Scientific, for example, signed a 12-year contract with AI-focused cloud computing provider CoreWeave that will see Core provide 200 MW of infrastructure to host CoreWave’s HPC services (the deal was later amended to add an additional 70 MW). In addition, Hut 8 secured $150m in funding from Coatue Management to build out its HPC vertical to support AI applications.

Hyperscale Data Center Market Size, $b

Source: Precedence Research, GSR.

Regulatory Items Paint a Mixed Picture

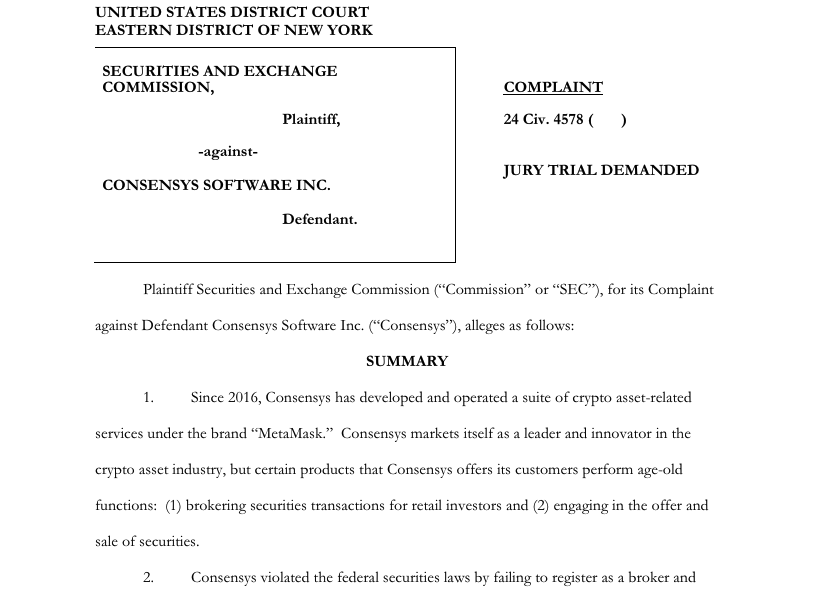

June saw many notable regulatory developments, with most emanating from the US and painting a mixed picture. Positively, the SEC closed its investigation into Ethereum 2.0 and will not bring charges against Ethereum development company Consensys for allegedly selling unregistered securities in the form of ETH. Further, the US Supreme Court ruled that securities fraud defendants should be granted a trial by jury in a federal court rather than using the SEC’s internal judicial process, which could temper the SEC’s enforcement powers. Lastly, it was revealed that the Biden administration, key congressmen, and digital asset industry leaders will meet in July to discuss ways to promote Bitcoin and blockchain innovation in the US. However, other regulatory-related events were more mixed. For example, though President Biden expressed a desire to develop digital asset legislation, he followed through on his promise to veto a measure that would have overturned the SEC’s controversial crypto custody accounting policy, SAB 121. And despite dropping its Ethereum 2.0 investigation and approving the recent spot Ethereum ETF 19b-4 filings as commodity-based trust shares, the SEC has not explicitly stated that Ethereum is a non-security commodity, even when directly asked. Additionally, while the US Supreme Court overturning the Chevron Doctrine to transfer power from the agencies to the courts when interpreting laws may reduce SEC power, this will actually make it harder to enact digital assets legislation as keeping language ambiguous to leave final decisions up to the regulator is the most common tactic to find bipartisan compromise and is now off the table. And while a US court dismissed claims relating to BNB secondary market sales / BUSD stablecoin sales and Binance’s passive income feature Simple Earn, it did rule against Binance’s attempt to dismiss the majority of claims made against it by the SEC. Finally, other items were more negative, with the SEC suing Consensys after alleging that its MetaMask wallet is an unregistered broker and that stETH and rETH are securities. And the US Department of Justice sentenced two individuals for manipulating the price of HYDRO marking the first time that a jury in a federal criminal trial found that a token is a security.

Outside of the US, notable regulatory-related news includes: The Financial Stability Board revealed plans to undertake work around stablecoin risks; MiCA’s stablecoin rules went in force; Dubai updated its crypto regulations; an Indian high court ruled that crypto dealings are not illegal; South Korea issued virtual asset guidelines for NFTs; South Korean crypto exchanges and a crypto trade association announced new self-regulatory standards; digital asset firms in Taiwan created new self-regulatory standards; and Bolivia’s central bank lifted its ban on cryptocurrency trading and payments.

The SEC’s Complaint against Consensys

Source: SEC.gov, GSR.

GSR in the News

- Fortune – Bain Capital Crypto leads $35 million Series A for M^0, a network for minting digital dollars

- The Block – Bain Capital Crypto leads $35 million Series A for M^0, a network for minting digital dollars

- Bloomberg – Crypto Market Maker GSR Names Rosenblum, Song as Co-CEOs

- The Block – GSR names co-CEOs as Jakob Palmstierna becomes company president

- The Block – Market maker GSR goes long on SOL, expecting it to outperform BTC

- Cointelegraph – Spot Solana ETF might 9x the price of SOL

- Unchained Crypto – Solana Has Cemented Itself in ‘Crypto’s Big Three’: GSR

- Cryptonews – SOL Price Could Increase by 9x after Spot Solana ETFs Approval, Predicts GSR Markets

- CryptoGlobe – Major Crypto Trading Firm GSR Longs Solana ($SOL), Says Spot ETF ‘Likely Just a Matter of Time’

- Bloomberg – US Reclaims Crypto Crown on Bitcoin ETFs, Trump Rise in Polls

- Bloomberg – Some of the Most-Hyped Crypto Tokens Are Performing the Worst

- Coindesk – Solana ETFs and Huge SOL Gains a Real Possibility Under Trump, Major Crypto Trader Says

- The Block –Market maker GSR goes long on SOL, expecting it to outperform BTC

- Cointelegraph – Spot Solana ETF might 9x the price of SOL — GSR Markets

- Decrypt – Solana ETFs Could Beat Bitcoin Gains, Be Fast-Tracked in Trump Admin: GSR

- Blockworks – Crypto Hiring: Industry trading giant now has 2 CEOs

Author:

Brian Rudick, Senior Strategist | Twitter, Telegram, LinkedIn

This material is provided by GSR (the “Firm”) solely for informational purposes, is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material. GSR is not authorised or regulated in the UK by the Financial Conduct Authority. The protections provided by the UK regulatory system will not be available to you. Specifically, information provided herein is intended for institutional persons only and is not suitable for retail persons in the United Kingdom, and no solicitation or recommendation is being made to you in regards to any products or services. This material is not a research report, and not subject to any of the independence and disclosure standards applicable to research reports prepared pursuant to FINRA or CFTC research rules. This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm trades instruments discussed in this material for its own account, may trade contrary to the views expressed in this material and may have positions in other related instruments.Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.